Can I retire at 45? This dream of financial freedom, travel, and more time with loved ones before 50 is becoming a reality for many millennials and Gen Zers thanks to the growing popularity of the Financial Independence, Retire Early (FIRE) movement. This guide explores the feasibility of retiring at 45, debunks common myths, and provides practical strategies to make this goal achievable.

Understanding the Path to Early Retirement

The FIRE Movement: A Modern Approach to Retirement

The FIRE movement encourages individuals to aggressively save and invest, allowing them to retire much earlier than the traditional retirement age of 65. This lifestyle shift emphasizes financial discipline, reducing unnecessary expenses, and maximizing savings. According to a 2022 survey, the FIRE movement has gained significant traction, with a growing number of millennials and Gen Zers embracing its principles. This trend is fueled by a desire for financial freedom and the growing awareness of early retirement strategies.

The FIRE movement encompasses various sub-categories, such as “Lean FIRE” (emphasizing extreme frugality), “Fat FIRE” (targeting a higher income level), and “Coast FIRE” (aiming to reach a point where passive income covers living expenses). For example, [name], a [profession] who retired at [age] with [amount] in savings, demonstrates how the FIRE principles can be applied to achieve early retirement.

Financial Independence vs- Traditional Retirement

Financial independence means having enough savings and investments to support your lifestyle without relying on a traditional job. While traditional retirement often involves a gradual withdrawal from the workforce, financial independence allows for a more immediate and potentially radical shift in lifestyle. This greater sense of control over your time and pursuits can be incredibly liberating, enabling you to explore new opportunities, pursue passions, and spend more time with loved ones.

Myth Busting: Early Retirement Doesn’t Require Millions

Many believe that retiring at 45 necessitates having millions in the bank, but this is a common misconception. With careful planning, disciplined saving, and smart investing, it is possible to retire early without accumulating vast wealth. The amount of savings required for early retirement depends heavily on your desired lifestyle. A minimalist lifestyle with lower expenses will necessitate a smaller savings goal compared to a more extravagant lifestyle.

Compounding, the snowball effect of earning interest on your interest, can significantly accelerate your wealth accumulation over time. For example, [name], a [profession] who retired at [age] with [amount] in savings, demonstrates that early retirement can be achieved with a strategic approach and a focus on maximizing the power of compounding.

Setting Realistic Expectations for Early Retirement

While retiring at 45 is achievable, it’s crucial to acknowledge the challenges and potential drawbacks. Potential challenges include feelings of boredom, difficulty transitioning out of the workforce, and the need for continued learning and self-motivation. It’s essential to remain flexible and adaptable, as unforeseen circumstances or changes in your personal priorities may require adjustments to your retirement plans.

Can I Retire at 45? Defining Your Retirement Vision and Goals

What Does Early Retirement Mean to You?

Your retirement vision is unique to you, reflecting your personal values, passions, and aspirations. It’s not about simply reaching a specific age or accumulating a certain amount of money; it’s about creating a fulfilling and meaningful life on your own terms. Some individuals may envision traveling the world, while others may prefer to pursue creative endeavors, start a business, or dedicate their time to volunteering.

Creating a “retirement bucket list” can help you visualize your ideal lifestyle and prioritize your goals. This list can include travel destinations, hobbies you want to pursue, or personal projects you want to undertake.

Envisioning Your Ideal Retirement Lifestyle

Your choice of location can significantly impact your expenses and lifestyle. Consider factors like cost of living, climate, and access to amenities when deciding where you want to retire. Additionally, think about the activities and hobbies you want to pursue, as well as the amount of time you want to devote to travel and leisure.

Determining Your Income Needs

Calculating your expected expenses in retirement is crucial. Consider factors like housing, healthcare, food, travel, and entertainment. Remember to factor in the impact of inflation, which can erode the purchasing power of your savings over time. Using online tools or consulting with a financial advisor can help you estimate your future expenses more accurately.

Addressing the Challenges of Early Retirement

Healthcare costs can be a significant concern for early retirees, especially before becoming eligible for Medicare. Explore options like individual health insurance plans, health savings accounts (HSAs), or alternative healthcare models to address this challenge. Additionally, consider ways to maintain social connections, such as joining clubs, volunteering, or pursuing hobbies that allow you to connect with others and maintain a sense of community.

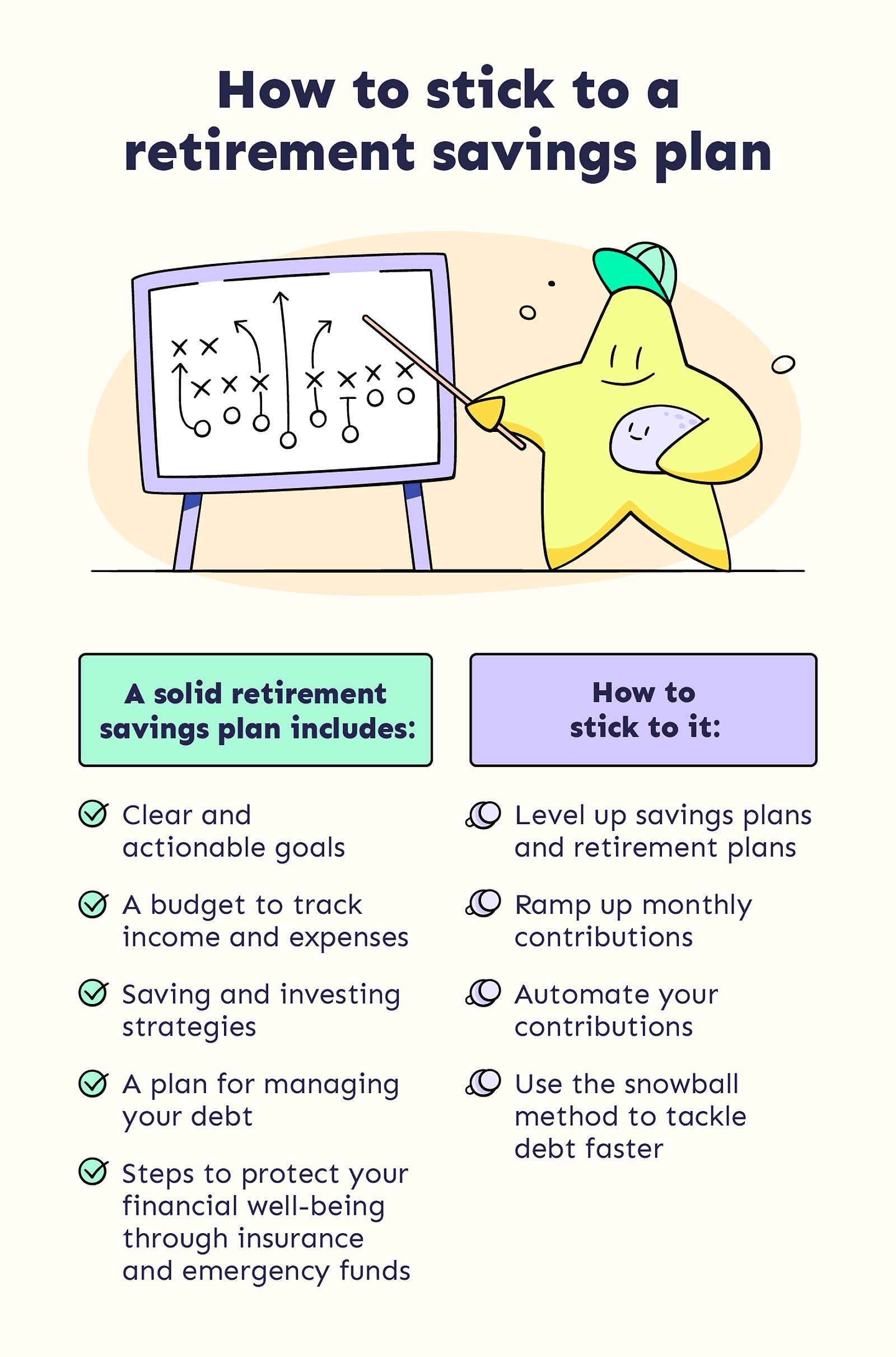

Building a Solid Financial Foundation

Maximizing Your Retirement Savings

Start by taking full advantage of retirement accounts such as 401(k)s and IRAs. These accounts offer tax advantages that can help your money grow faster. If your employer provides a matching contribution, ensure you contribute enough to receive the full match — this is essentially free money that can significantly boost your retirement savings. Consider the benefits of Roth 401(k)s, which offer tax-free withdrawals in retirement.

Understanding Retirement Savings Accounts: 401(k)s, IRAs, and Roth IRAs

| Account Type | Contribution Limits | Tax Implications | Withdrawal Rules |

|---|---|---|---|

| 401(k) | $19,500 (2021) | Pre-tax contributions | Penalties for early withdrawal |

| Traditional IRA | $6,000 (2021) | Pre-tax contributions | Penalties for early withdrawal |

| Roth IRA | $6,000 (2021) | After-tax contributions | Tax-free withdrawals in retirement |

Smart Investing Strategies

Focus on creating a diversified investment portfolio that aligns with your risk tolerance and long-term goals. A balanced mix of stocks, bonds, and real estate can help protect your investments from market volatility and lead to more stable long-term growth. Work with a financial advisor to develop an investment strategy that suits your needs.

Practical Tips for Increasing Savings

- Automate your savings contributions to ensure consistency and avoid the temptation to spend the money elsewhere.

- Identify areas where you can cut back on expenses, such as negotiating lower cable bills or finding more affordable housing options.

- Consider negotiating for a higher salary to boost your savings potential.

Navigating the Financial Landscape

Minimizing Taxes and Optimizing Retirement Accounts

Early retirees may face unique tax challenges, such as penalties for withdrawing from retirement accounts before age 59.5. Strategies like tax-loss harvesting and carefully timing your withdrawals can help minimize your tax liability. Consulting with a tax professional can provide valuable insights and ensure you’re taking advantage of all available tax-saving opportunities.

Finding the Right Financial Advisor

Working with a qualified financial advisor can provide the expertise needed to create a personalized retirement plan. Look for advisors with reputable designations, such as Certified Financial Planner (CFP) or Chartered Financial Analyst (CFA), and establish a strong advisor-client relationship based on trust, communication, and shared goals.

Frequently Asked Questions

What if I don’t have a steady income?

Even if you don’t have a traditional job, it’s possible to achieve early retirement by developing alternative income streams, such as freelancing or starting a small business. The key is to diversify your income sources and maintain a disciplined savings and investment strategy.

Can I retire early if I have a family?

Yes, but you’ll need to account for additional expenses like childcare and education when planning your retirement budget. Effective budgeting and a focus on saving and investing can help you achieve early retirement even with a family.

What are the psychological aspects of early retirement?

Leaving the workforce early can be a significant transition, both financially and emotionally. It’s essential to prepare for potential feelings of boredom, isolation, or lack of purpose. Maintaining social connections, pursuing hobbies, and finding ways to stay mentally and physically active can help you navigate the psychological aspects of early retirement.

How can I stay motivated to reach my retirement goals?

Set clear and achievable milestones along the way to track your progress. Celebrate small victories and remind yourself of the long-term benefits of early retirement. Staying connected with like-minded individuals in the FIRE community can also provide inspiration and support.

Conclusion

Retiring at 45 is an ambitious yet achievable goal for millennials and Gen Zers who are willing to embrace a disciplined approach to saving, investing, and financial planning. By defining your retirement vision, calculating your financial needs, and building a solid financial foundation, you can take control of your future and achieve financial independence on your own terms. Remember to stay informed, seek professional guidance, and remain flexible as you navigate the journey towards early retirement. The dream of a life free from the constraints of a traditional 9-to-5 job is within reach — take the first step today.